AI-generated summary

In 2024, Spain’s startup investment landscape has seen significant transformation, marked by a 38% growth in total investment volume during the first nine months compared to 2023. This surge is predominantly driven by mega rounds—investments exceeding €50 million—which now represent 55% of total startup funding and reflect heightened international investor confidence. Despite a drop in the number of funding rounds by 8%, the average round size increased to €8.4 million, signaling a focus on larger, more mature ventures. However, early-stage startups face funding challenges, evidenced by a 16% decline in the median round size to €1 million and fewer Preseed/Seed and Series A rounds. Public investment has rebounded by 24%, while local investors remain active, though foreign investors dominate the economic volume, often backing later-stage startups.

Sector-wise, Fintech/Insurtech leads with 28% of total investment, followed by Travel & Tourism and Mobility & Logistics, reflecting shifting market opportunities. Key funding highlights include Zunder’s €225 million round for ultra-fast electric vehicle charging, Boopos’s €175 million marketplace launch, and ID Finance’s €140 million digital banking development. Regionally, Barcelona and Madrid remain top hubs, with Palencia rising due to Zunder’s investment. The year also shows robust exit activity, with 48 deals closed to date and notable transactions like HG Capital’s €160 million acquisition in contractor management software. Overall, despite fewer deals, the increased investment size and strong international participation signal a promising recovery for Spain’s entrepreneurial ecosystem in 2024.

The startup investment market has grown significantly in 2024, driven by interest in more advanced projects.

In the world of startup investment, 2024 has brought several pieces of news. Mega rounds, emerging sectors and renewed confidence from international investors are driving this transformation. Although the big stakes have increased, early-stage investment faces challenges. Discover the figures and trends that shape entrepreneurship in Spain.

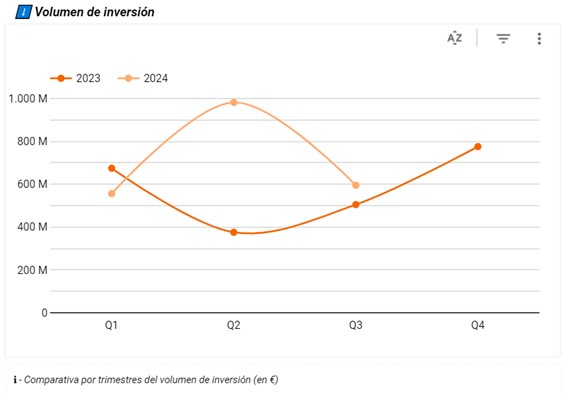

Investment volume

The total investment volume has grown by 38% in the first nine months of 2024 compared to the same period in 2023. Given that 92% of the total invested during the whole of 2023 has already been reached, a higher figure is anticipated to close the year.

This growth is largely explained by the increase in mega rounds, those of more than 50 million euros, and which often include the participation of international investors.

If these mega rounds are not considered, an 8% decrease in investment volume and an 11% drop in the number of operations are observed. So far in 2024, mega rounds account for 55% of the total amount of investment in startups.

The number of operations has decreased by 8% compared to the first 9 months of 2023.

There has been a 38% increase in the average amount of the rounds, reaching 8.4 million euros. This situation is due to the decrease in the number of operations, combined with an increase in the volume of investment. This is clearly influenced by the increase in mega rounds.

Despite the upward trend in investment volume, the median of rounds has fallen by 16% to €1 million, which shows a higher proportion of smaller rounds. This reflects a decrease in funding for early-stage startups.

However, the increase in the volume of economic investment could be a sign of economic recovery in the startup funding ecosystem after the last two years of decline. The start of the interest rate cut in 2024 may lead to a renewed flow of capital towards projects with higher profitability and risk, by improving the IRR of operations with startups.

The year started with a 17% drop in investment during the first quarter, but the second quarter saw a marked improvement, with a 161% increase. The third quarter showed moderate growth, with a 22% increase in funds raised by startups.

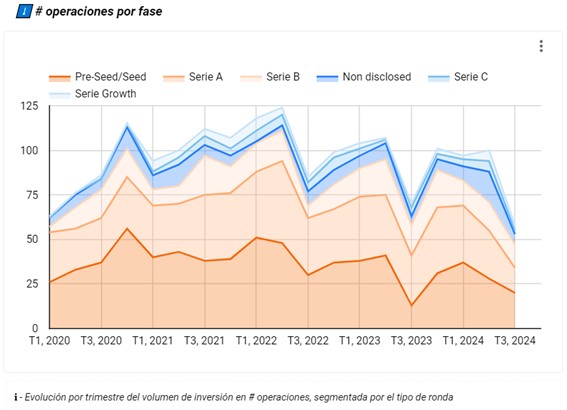

Types of investment rounds

Comparing the first three quarters of 2024 compared to the same period last year, an increase in the number of Series C and Series Growth rounds has been observed, which have gone from 11 to 13 and from 6 to 11 respectively. However, other round categories have seen a decline: Preseed/Seed rounds have gone from 92 to 85, Series A from 98 to 73, and Series B from 53 to 43. These trends show a growing interest in projects in more mature phases.

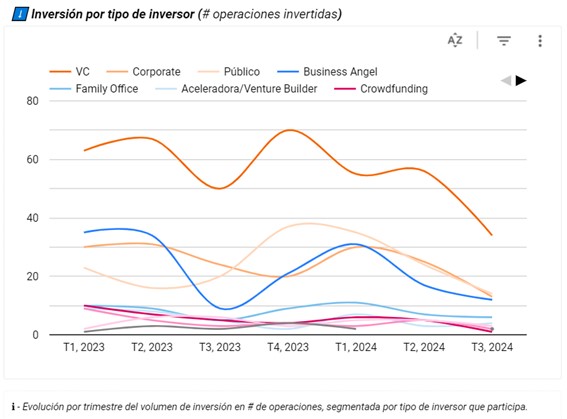

What type of investors have been most active?

Analysis of investment activity shows a slight decline in the participation of the main types of investors during the first nine months of 2024. On the positive side, public investment rebounded, increasing by 24% in the first 9 months of 2024 compared to the same period of the previous year.

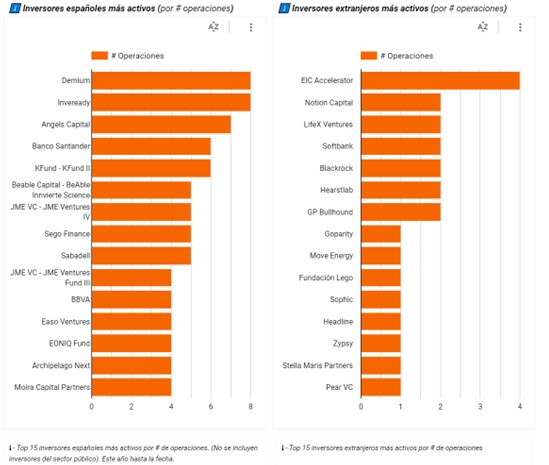

Among the most active local investors, the following stand out:

- Demium and Inveready, with 8 operations each

- Angels Capital with 7 operations

- Banco Santander and K-Fund, which have carried out 6 operations each

At the international level:

- EIC Accelerator, European public vehicle, with 4 operations

- Notion Capital, LifeX Ventures, Softbank, BlackRock, Hearstlab, and GP Bullhound, each with 2 operations.

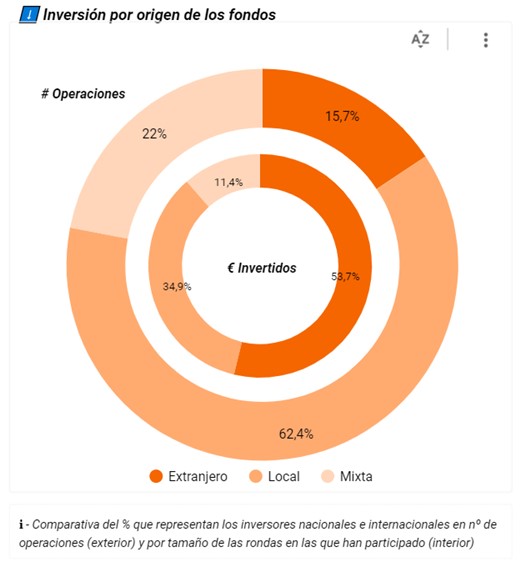

In the first 9 months of 2024, the number of rounds in which exclusively local investors participate represent the majority of operations, with 62% of the total. However, 54% of the economic volume of investment corresponds to rounds in which exclusively foreign investors participate, who tend to invest in more mature phases and, therefore, in larger rounds.

Regarding the volume of investment according to the nationality of investors, it can be seen that rounds financed solely by foreign investors have reached 134% of the total invested in all of 2023 in this category. This is a very positive figure that shows that international investors show confidence in the Spanish entrepreneurial ecosystem.

In contrast, mixed rounds, where foreign and national investors co-invest, have decreased, standing at 27% of the investment registered last year in this type of rounds during the first 3 quarters of the year. Local investment registers the same volume in the first nine months of the year as in the whole of last year.

The sectors in which there is more activity

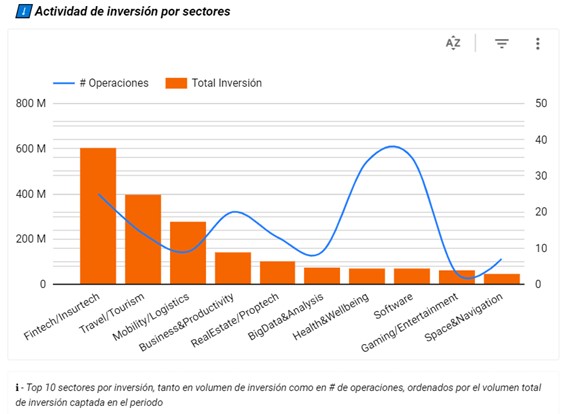

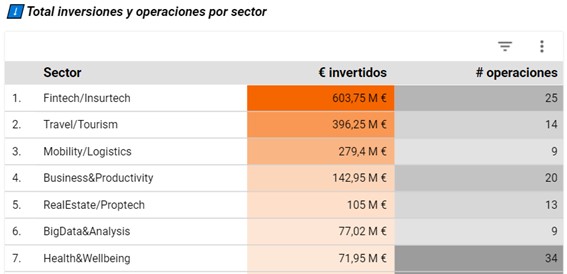

The Fintech/Insurtech sector is standing out in 2024, accounting for 28% of total investments in startups and attracting €603 million in the first 3 quarters of the year.

Other sectors that also show promising prospects are Travel & Tourism, which is in second place with €396 million, driven by the favourable global forecasts for tourism derived from changes in consumption habits and financial situation in developed countries. The third position in the financing ranking is occupied by the Mobility & Logistics sector, with 279 million euros raised.

Which companies have you invested in?

The most prominent operation is Zunder, the benchmark ultra-fast charging operator for electric vehicles in southern Europe. The Palencia-based company has raised 225 million euros.

In second place is Boopos, the new project Juan Ignacio García Braschi (co-founder of Cabify), which has attracted 175 million euros of investment. Boopos is a marketplace where small digital businesses are bought and sold, has a team in Madrid and Miami, and has tax headquarters in the United States. Boopos differentiates itself from its competitors by additionally offering the financing needed to carry out the underlying transactions.

In third place is Barcelona-based ID Finance, which develops digital banking services, and has secured a €140 million funding round.

How investment is distributed throughout Spain

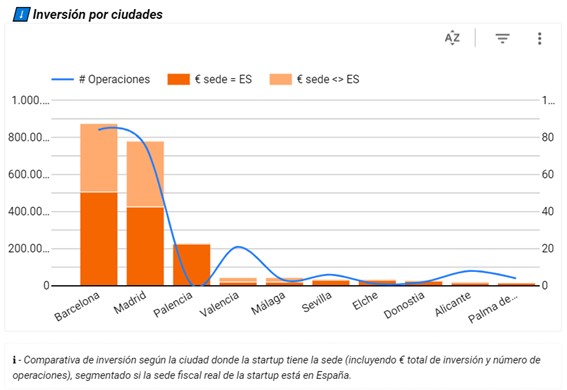

On the map of Spanish entrepreneurship, Palencia has gained prominence by occupying third place in attracting investment, thanks to the outstanding operation of Zunder, which has raised 225 million euros. Barcelona leads the national entrepreneurship hubs with 874 million and Madrid follows with 780 million.

Divestitures (EXITS)

Exits activity in 2024 has begun with intense buying activity. In 2023, 53 operations were closed, and so far in 2024 48 have already been completed, representing 90% of the total for 2023.

In the third quarter of 2024, the most significant transaction was carried out by the British fund HG Capital, which acquired nearly 50% of the group resulting from the merger of Ctaima and E-Coordina, valuing the combined company at €160 million. This investment seeks to create a leading software platform in Europe for contractor management, risk and compliance, integrating the capabilities of both companies and positioning itself as a benchmark in Europe.

In conclusion, the volume of investment in startups has grown in 2024, driven by mega rounds and increased interest from international investors. Although operations have decreased, the increase in the average amount and foreign confidence suggest an economic recovery in the entrepreneurial ecosystem.