AI-generated summary

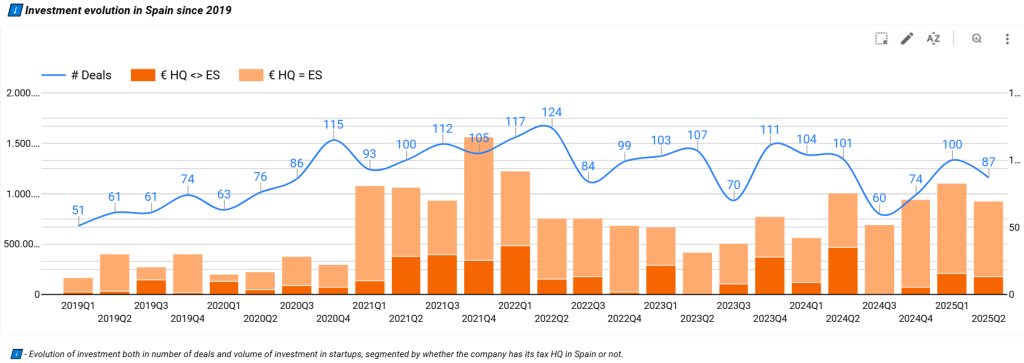

In the first half of 2025, Spanish startups demonstrated robust growth by raising over €2 billion in funding—a 23% increase from the same period in 2024—despite an 11% decline in the number of deals to 187. This surge in capital was concentrated mainly in later-stage rounds (Series C and Growth), which accounted for 15% of deals but captured 78% of total investment (€1 billion+). Venture capital funds were the predominant investors, participating in 69% of deals, followed by public institutions, corporates, and business angels. Leading sectors attracting significant funding included Software (€395M), Travel & Tourism (€345M), and Business & Productivity (€257M). Notable large rounds featured Multiverse Computing (€67M and €189M), TravelPerk (€190M), and SpliceBio (€110M). Geographically, Barcelona emerged as the key investment hub, hosting 33% of deals and 47% of capital (€955M), ahead of Madrid and San Sebastián.

The ecosystem’s maturation is evident in the preference for more mature startups with proven business models, fueled by central bank interest rate cuts that enhance venture capital attractiveness. Early-stage rounds (Pre-seed to Series A) declined slightly but remain vital for sustaining future growth. Investor diversity increased, with a mix of equity, debt, and public subsidies optimizing financing structures. Exits slowed to 24 in H1 2025 but included impactful events such as Hotelbeds’ IPO (€2.84 billion valuation) and major acquisitions, signaling ongoing liquidity opportunities. Overall, Spain’s startup landscape is evolving rapidly, driven by AI innovation and strategic investor involvement, positioning it strongly for future expansion.

Key highlights Investment Volume The first half of 2025 brought positive momentum to the Spanish startup ecosystem. Total fundraising surpassed €2.000 million, representing a 23% increase over the same period in 2024. This fact aligns with central banks’ interest rate cuts, increasing liquidity and making risk capital like venture capital more attractive compared to traditional […]

Key highlights

- Spanish startups raised over €2.000 million in the first half of 2025, marking a 23% increase compared to the same period in 2024, despite an 11% drop in the number of deals (187 rounds).

- Series C and Growth rounds accounted for 26 deals (15% of the total), capturing over €1.000 million, representing 78% of total capital invested.

- VC funds were involved in 69% of all rounds, the next most relevant investor stakeholders are public institutions, corporates, and Business Angels.

- Top funded sectors: Software (€395M), Travel & Tourism (€345M), and Business & Productivity (€257M), each recording rounds exceeding €100 million.

- Largest Rounds: Multiverse Computing (two rounds of €67M & €189M), TravelPerk (€190M), and SpliceBio (€110M) led the rankings.

- Barcelona as the Investment Hub: Barcelona led with 33% of deals and 47% of total capital (€955M), followed by Madrid (€527M) and San Sebastián (€261M).

- Exits: 24 exits occurred in Q1 2025, fewer than in 2024, but included high-impact deals such as Hotelbeds’ IPO.

Investment Volume

The first half of 2025 brought positive momentum to the Spanish startup ecosystem. Total fundraising surpassed €2.000 million, representing a 23% increase over the same period in 2024.

This fact aligns with central banks’ interest rate cuts, increasing liquidity and making risk capital like venture capital more attractive compared to traditional financial instruments with declining yields.

However, the capital raised was concentrated in fewer transactions, 187 in total, an 11% drop from the first half of 2024. Average and median deal sizes rose to €12M and €2M, respectively, signaling investors’ preference for more mature startups with higher ticket sizes.

This trend reflects growing investor appetite for de-risked opportunities: companies with proven business models and established go-to-market strategies are favored, especially in volatile tech and economic climates.

The startup ecosystem is undergoing a transformation driven by the surge in artificial intelligence. Startups are increasingly leveraging AI agents and techniques such as vibe coding to accelerate product development. Yet, these AI-driven startups face two critical challenges to ensure long-term viability:

- Proving a unique and differential business model that offers real value beyond incremental enhancements from LLMs like ChatGPT, Gemini, or Claude.

- Establishing an effective distribution network that ensures sustainable and profitable customer acquisition, maximizing the impact of their value proposition.

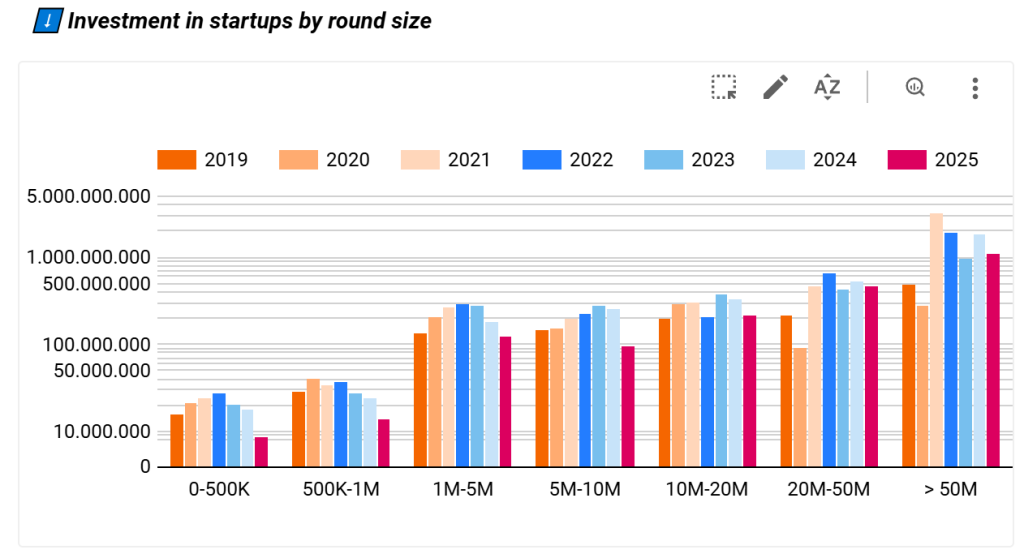

Investment by Stage

- Pre-seed: Pre-seed: Only 7 deals (≤€100K each), representing 4% of the total. The low number is partly due to limited media visibility and undisclosed deal sizes at this stage.

- Seed and Series A: Accounted for over 100 rounds, 58% of total deal volume, but both experienced a decline between 10–20%. Support at these early stages is crucial to ensure a steady pipeline of potential scaleups.

- Series C and Growth: These later-stage rounds gained momentum with 28 deals (15% of total), up from 19 last year. Investment in these stages exceeded €1.500 million, 77% of total capital, highlighting their growing relevance. Series C rounds grew by 55%, and Growth rounds by 22%.

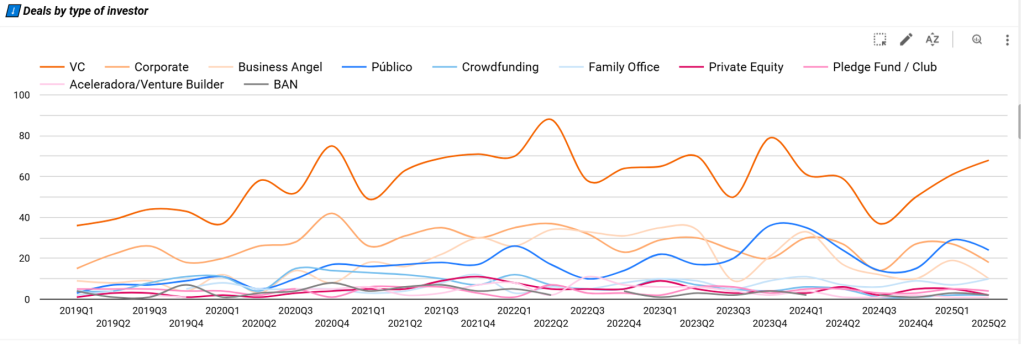

Most Active Investor Types

In H1 2025, Venture Capital funds were the most active backers, participating in 69% of all deals in Spain.

Public institutions such as ENISA, CDTI, and the EIC consolidated their position as the second most active investor type, participating in 53 deals. Their involvement has grown notably. These entities often complement private capital in funding rounds, bringing stability, trust, and helping attract private investment.

Corporates were the third most active, with 45 deals. They typically invest strategically in startups related to their sector.

Business Angels participated in 29 rounds during the first half of the year. Their contribution is especially relevant at early stages, where risk is higher and access to funding more limited. Many are successful entrepreneurs reinvesting their experience, networks, and capital in new projects.

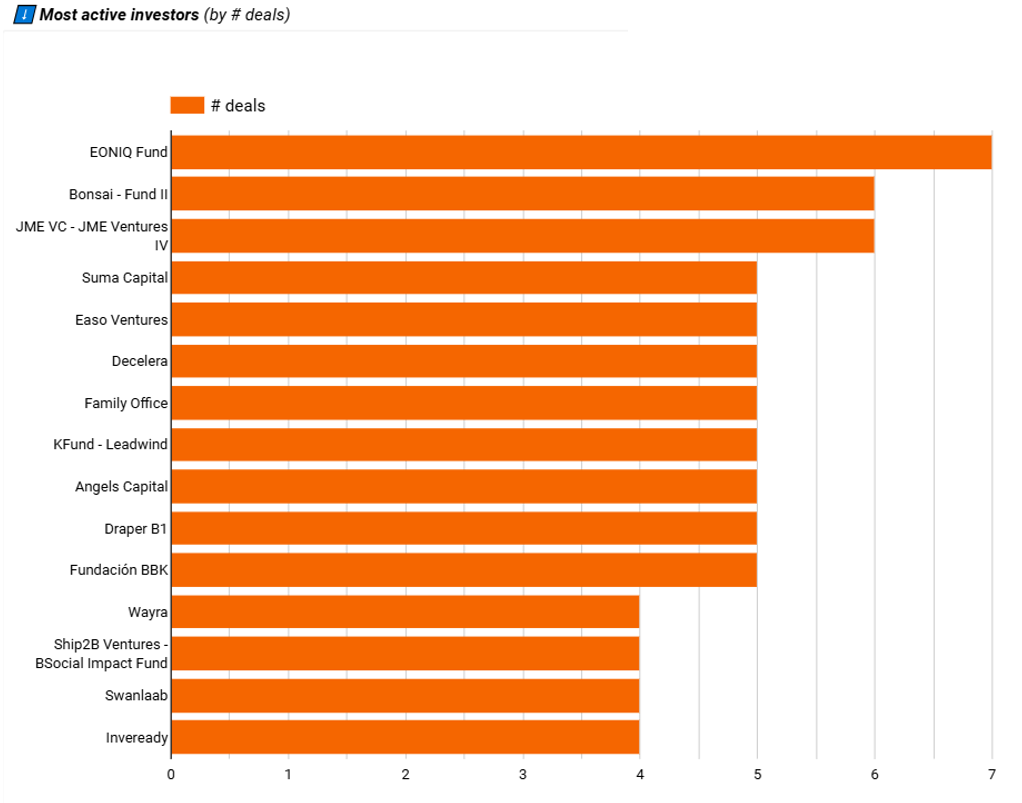

Most Active Investors by Number of Deals:

- Eoniq: A fund focused on early-stage tech startups, especially those outside Madrid and Barcelona.

- Bonsai Partners: Invests in European startups up to Series B.

- JME Capital: The fund linked to José Manuel Entrecanales, investing in Spanish startups.

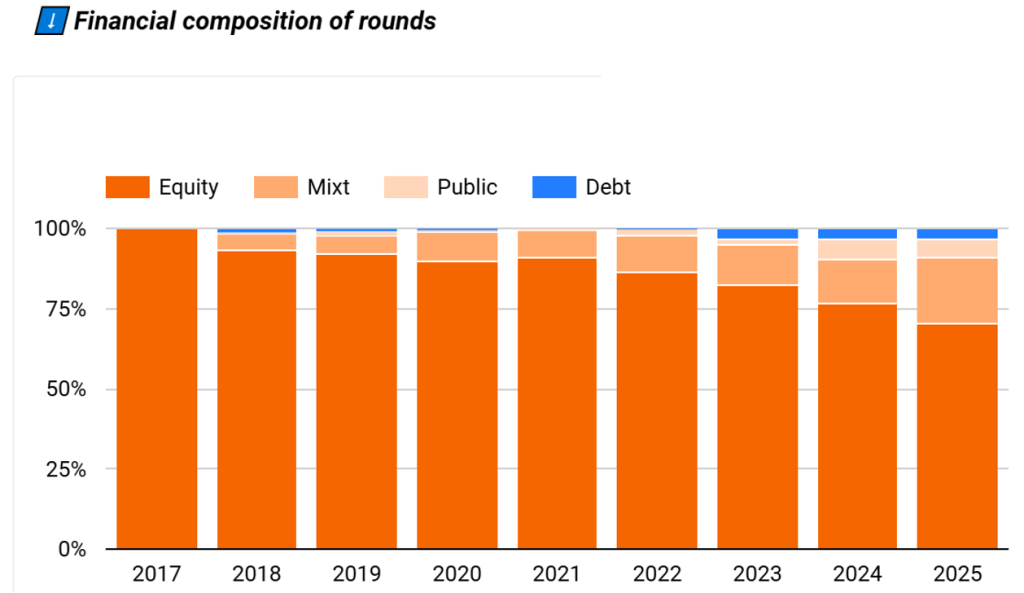

As a sign of the growing maturity of Spain’s startup ecosystem, investors are increasingly using a diverse range of financial instruments. Funding rounds no longer rely solely on equity; they increasingly include debt and public subsidies.

At early stages, startups often supplement equity investment with soft loans from public institutions. Mature startups more frequently use debt financing, taking advantage of their stronger cash flow generation.

This financial diversification is especially beneficial to entrepreneurs as it reduces equity dilution and optimizes financing costs (WACC).

Investor Location

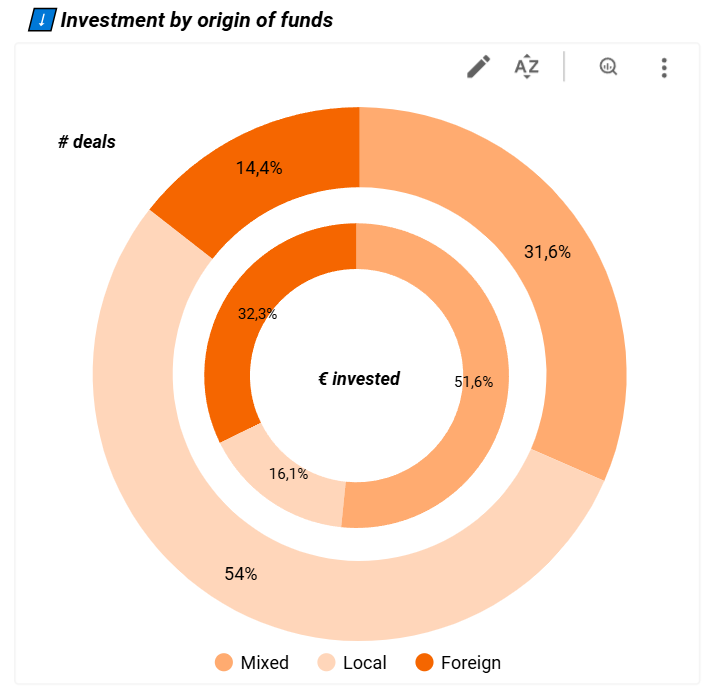

In 85% of all deals, at least one Spanish investor participated.

Deals funded exclusively by foreign investors declined by 7% in number and 42% in volume compared to H1 2024.

During the first half of the year, 59 mixed rounds were recorded, co-investments by Spanish and foreign funds, raising over €1.000 million, equivalent to 52% of total startup investment in Spain during H1 2025.

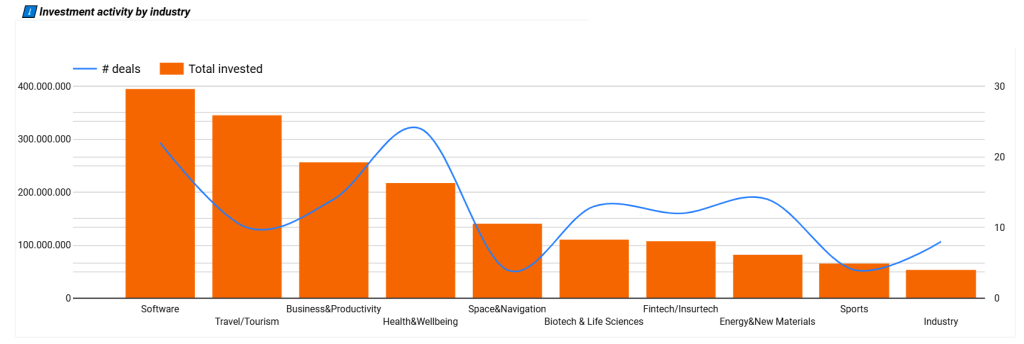

Most Active Sectors

The top investment sector was Software, attracting €395 million in 22 rounds in the first half of the year.

A standout was Travel & Tourism, with €345 million in 10 rounds, a significant increase over the previous year.

Third was Business & Productivity, with startups focused on streamlining and organizing business processes through technology raising €257 million in 14 rounds.

Most Relevant Rounds

Four of the five largest funding rounds belong to the most dynamic sectors mentioned above. The table below shows the details:

| Startup | City | Activity | Capital Raised (2025) | Lead Investor |

| Multiverse Computing | San Sebastián | Software solutions for AI and quantum computing | €67M (March) + €189M (June) | SETT y Bullhound Capital |

| TravelPerk | Barcelona | Corporate travel management platform | €190M | Atómico y EQT Partners |

| SpliceBio | Barcelona | Gene therapies using protein splicing for hereditary diseases | €119M | EQT Partners |

| Factorial | Barcelona | HR software for SMEs (payroll, time-off, time tracking, etc.) | €110M | General Catalyst |

| Jobandtalent | Madrid | Temporary staffing platform based on algorithms and matching | €92M | Blackrock |

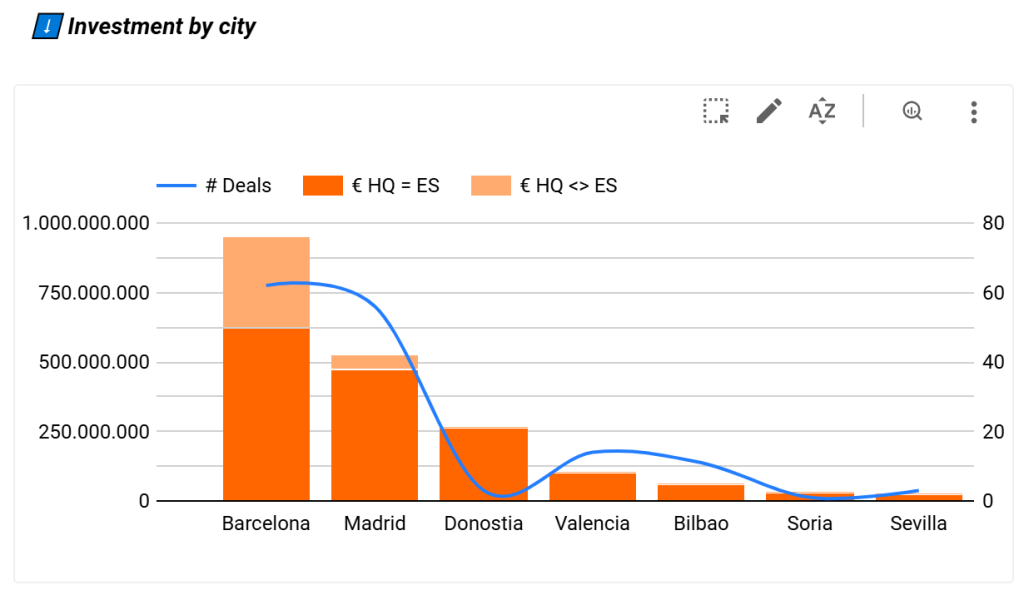

Investment Map: Where is Capital Moving?

Barcelona recorded 62 startup investment rounds in H1 2025, representing 33% of all Spanish deals. Collectively, its startups raised €955 million, a 27% increase over the same period last year. Highlights include rounds by TravelPerk, SpliceBio, and Factorial.

Madrid secured 56 deals totaling €527 million. Major rounds included Jobandtalent, Playtomic, and Xcalibur Smart Mapping.

San Sebastián came third, with just 3 investment rounds but a total of €261 million raised, primarily by Multiverse Computing, which raised €256 million from VC funds, corporations, public institutions, and Basque public funds.

Exits

A total of 24 exits were recorded in the first half of 2025, providing liquidity to founders and early-stage investors. Although this represents a 25% decline compared to the same period in 2024, several high-impact transactions occurred in different formats:

- IPO: Hotelbeds went public in February 2025 with a market capitalization of €2.840 million.

- Industrial Exit: Legaltech company vLex was acquired by Canadian firm Clio for €850 million.

- Private Equity: Digital marketing and communications agency Samy Alliance sold a majority stake to London-based PE fund Bridgepoint for €300 million.

- Startup M&A: Playtomic acquired Timp for approximately €7 million. This deal illustrates how mature startups are increasingly acquiring smaller players to grow inorganically and generate synergies.